Share this Post

TL;DR

Restricted Stock Units and bonuses typically face a flat supplemental withholding tax rate of twenty-two percent. High earners sit in much higher tax brackets. This gap often creates massive surprise tax bills and IRS underpayment penalties. You can fix the withholding gap to avoid penalties while using specific planning strategies to reduce your total tax burden.

The Bonus Check That Bounced At Tax Time

James, a mid-level product manager, experienced a massive wealth event last year. A large block of Restricted Stock Units vested in November. A significant cash bonus arrived in December. The bank account balance looked incredible. Financial security felt as good as it ever has. James used a portion of the funds to secure a down payment on a new house. Life moved forward smoothly until tax season arrived.

The annual meeting with a CPA brought terrible news. A forty-thousand-dollar tax bill was due. The IRS also tacked on an underpayment penalty. Total income was not the actual problem. The real issue centered entirely on how the employer handled tax withholding.

This story happens hundreds of thousands of times every spring (maybe even millions). High earners assume their employer handles tax withholding correctly. But employers follow baseline IRS rules.

You need a specific plan to avoid this trap.

Why Do RSUs and Bonuses Cause Huge Tax Bills?

The IRS treats regular salary differently from equity compensation and bonuses. Regular paychecks use standard withholding tables based on your W-4 form. The government classifies RSUs and cash bonuses as supplemental income.

Federal tax law requires companies to withhold a flat 22% tax on supplemental income up to $1 million. Income over one million dollars faces a 37% percent withholding rate. Most professionals fall under the one-million-dollar threshold.

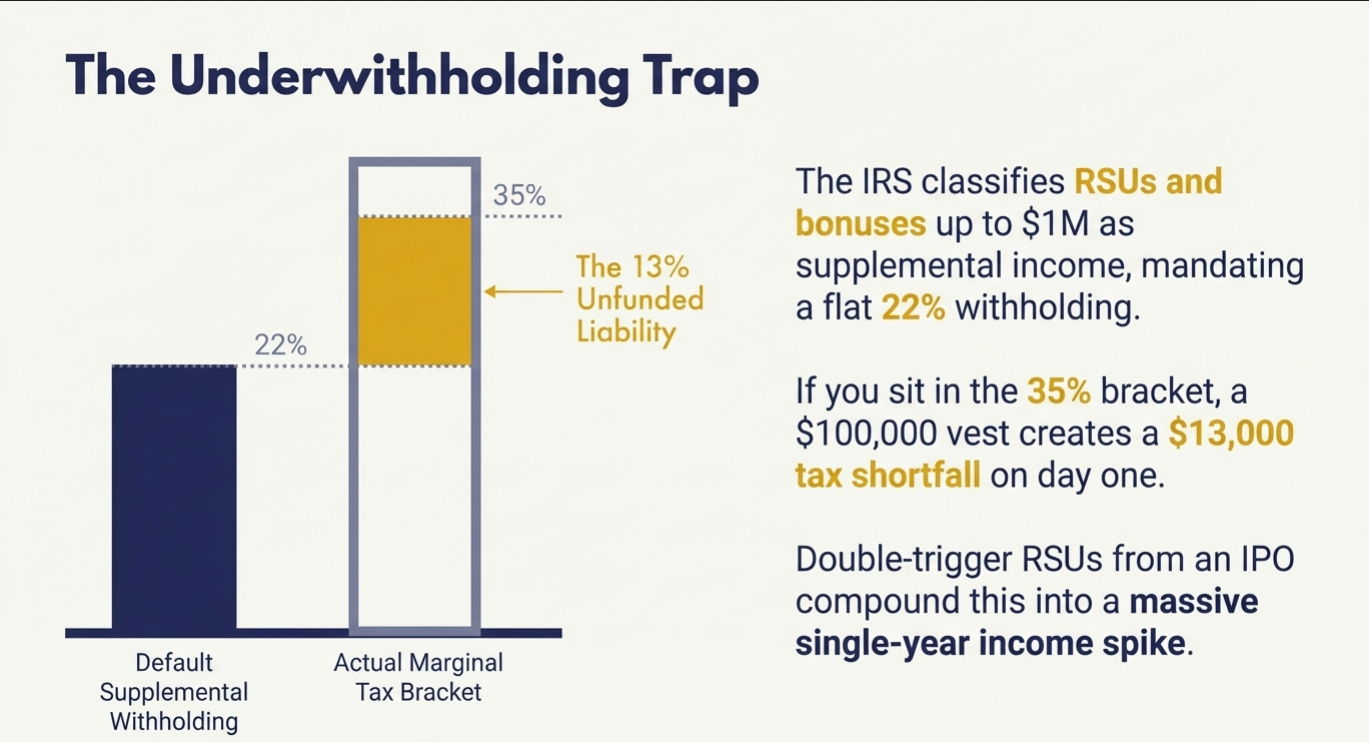

And that likely means you fall behind on taxes the moment the shares vest. A hundred thousand-dollar RSU vest generates twenty-two thousand dollars of tax withholding. An employee in the 35% bracket actually owes thirty-five thousand dollars on that vest. A thirteen-thousand-dollar shortfall exists.

Private company equity introduces another layer of risk. Double trigger RSUs require both a time-based vesting period and a liquidity event like an Initial Public Offering. An IPO causes years of accrued shares to vest all at once. This creates an enormous single-year income spike. The flat withholding rate can epicly fail in this scenario, and you could owe a massive amount of money the following April.

A comparative bar chart highlighting the equity tax trap for high earners. The key insight shows the unfunded liability gap between the default twenty two percent supplemental withholding rate and an actual thirty five percent marginal tax bracket.

This chart assumes hypothetical tax brackets. This does not constitute specific tax advice.

How Do We Avoid IRS Underpayment Penalties?

The IRS demands tax payments throughout the year as you earn income. Waiting until April to pay your shortfall triggers an underpayment penalty. You can avoid these penalties by following specific safe harbor rules.

The government provides clear thresholds for penalty protection. Taxpayers with an Adjusted Gross Income over one hundred fifty thousand dollars must pay one hundred ten percent of their previous year's tax liability. Taxpayers under that income level must pay one hundred percent of the previous year's liability. Meeting these safe harbor targets guarantees you will not face an underpayment penalty. But, very importantly, you might still owe taxes in April, but the penalty is waived.

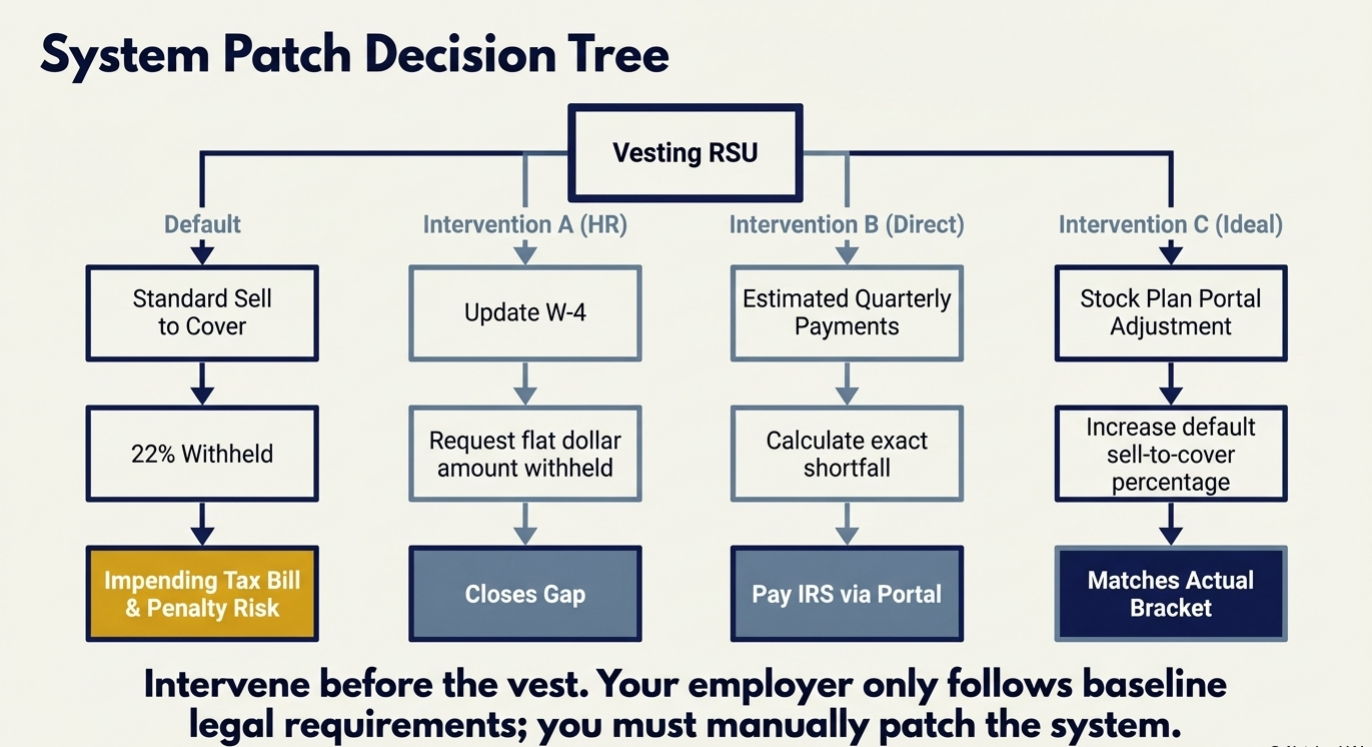

Closing the withholding gap requires proactive steps. You can update your W-4 form with your human resources department. This form allows you to request an additional flat dollar amount withheld from every regular paycheck. The extra cash helps cover the RSU shortfall.

Making quarterly estimated tax payments offers another solution. You calculate the shortfall after each vest. You then send a direct payment to the IRS through their website.

Some companies offer a better alternative. Check your stock plan administration portal. Certain employers allow you to elect a higher withholding percentage for RSU vests. You can change the default twenty-two percent rate to match your actual tax bracket.

*Keep in mind that tax laws change frequently. You should consult a tax professional before making significant changes to your withholding strategy.

A financial planning flowchart outlining actionable steps to avoid underpayment penalties on equity compensation. It contrasts the default sell to cover method with proactive strategies like adjusting paycheck withholdings or making estimated payments to reach safe harbor status.

For illustrative purposes only. Consult a qualified tax professional before modifying your withholding elections.

What Strategies Actually Lower the Tax Bill on RSUs?

Paying the correct amount of tax on time prevents penalties. Fixing your withholding does not actually reduce your total tax liability. You need specific wealth management strategies to keep more of your money.

Can Direct Indexing Offset Short-Term RSU Gains?

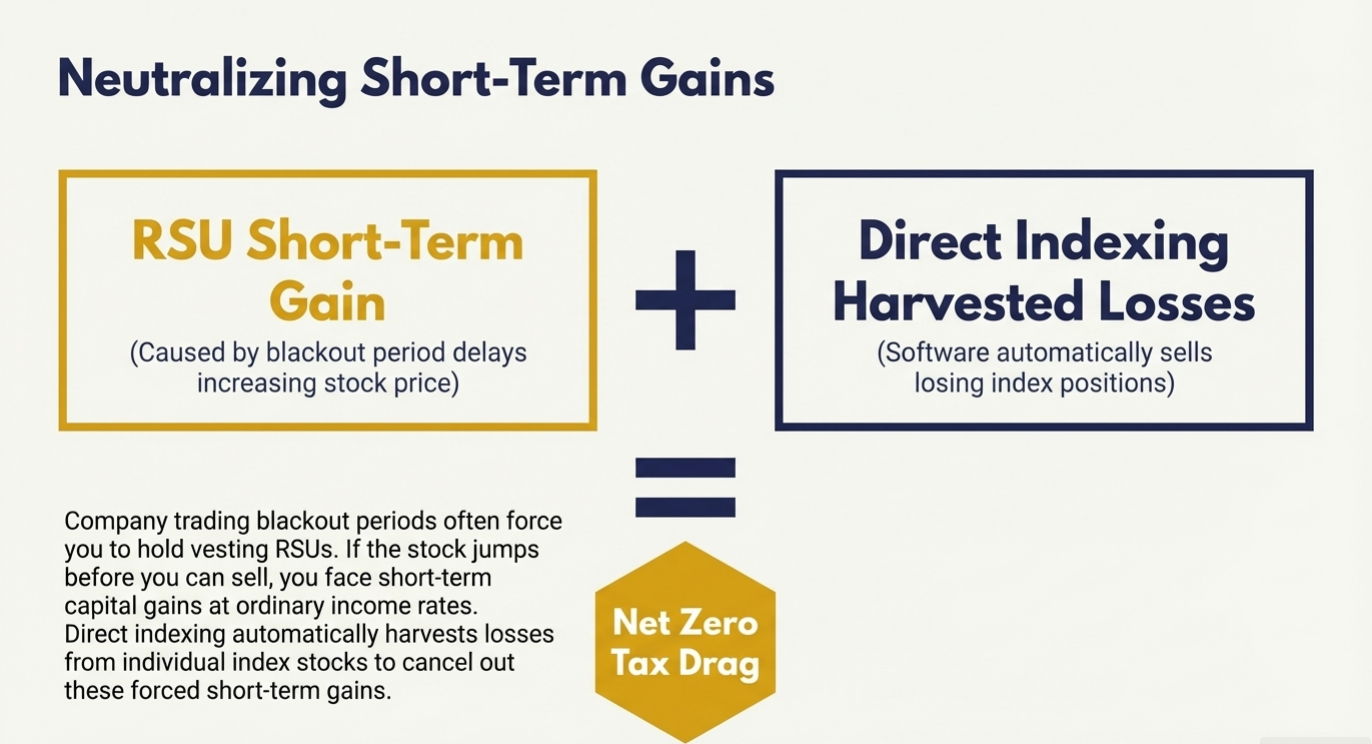

Professionals earning company stock, such as RSUs, often face trading blackout periods. You might want to sell your shares the day they vest. Company policy often prevents you from selling until the trading window opens a few days or weeks later.

The stock price might increase during this waiting period. So selling the shares now creates a short-term capital gain on the price bump. And short-term gains face ordinary income tax rates. This creates a hidden tax drag that silently reduces your wealth accumulation. As an aside, this dynamic is what mistakenly leads many people to believe that holding RSUs for one year after vesting generates tax benefits on the whole vested amount (this is not true).

If you have a large amount of RSUs vesting consistently, one strategy to explore for tax reduction is using direct indexing. Direct indexing involves owning the individual stocks of an index rather than a single Exchange Traded Fund. Then you ideally use software that automatically sells losing positions to harvest losses (it's a bit more involved, but that's the gist of it). These harvested short-term losses cancel out the short-term gains from your delayed RSU sales. You can read more about this exact approach in our guide The Hidden Tax Drag on Your RSUs and How Direct Indexing Could Help Fix It.

*Direct indexing does involve investment risk. The strategy requires holding stocks that may decline in value. Loss harvesting provides no benefit if your portfolio lacks losing positions. Market volatility can cause the entire portfolio to lose value. Past performance of direct indexing strategies does not guarantee future results.

A visual financial equation showing how systematic tax loss harvesting through direct indexing can offset short term capital gains caused by trading blackout periods. This original analysis illustrates how investors can create a net zero tax drag on their equity compensation.

Direct indexing involves market risk, including possible loss of principal. Tax loss harvesting does not guarantee a specific tax outcome.

How Does Maxing Out Pre-Tax Accounts Help?

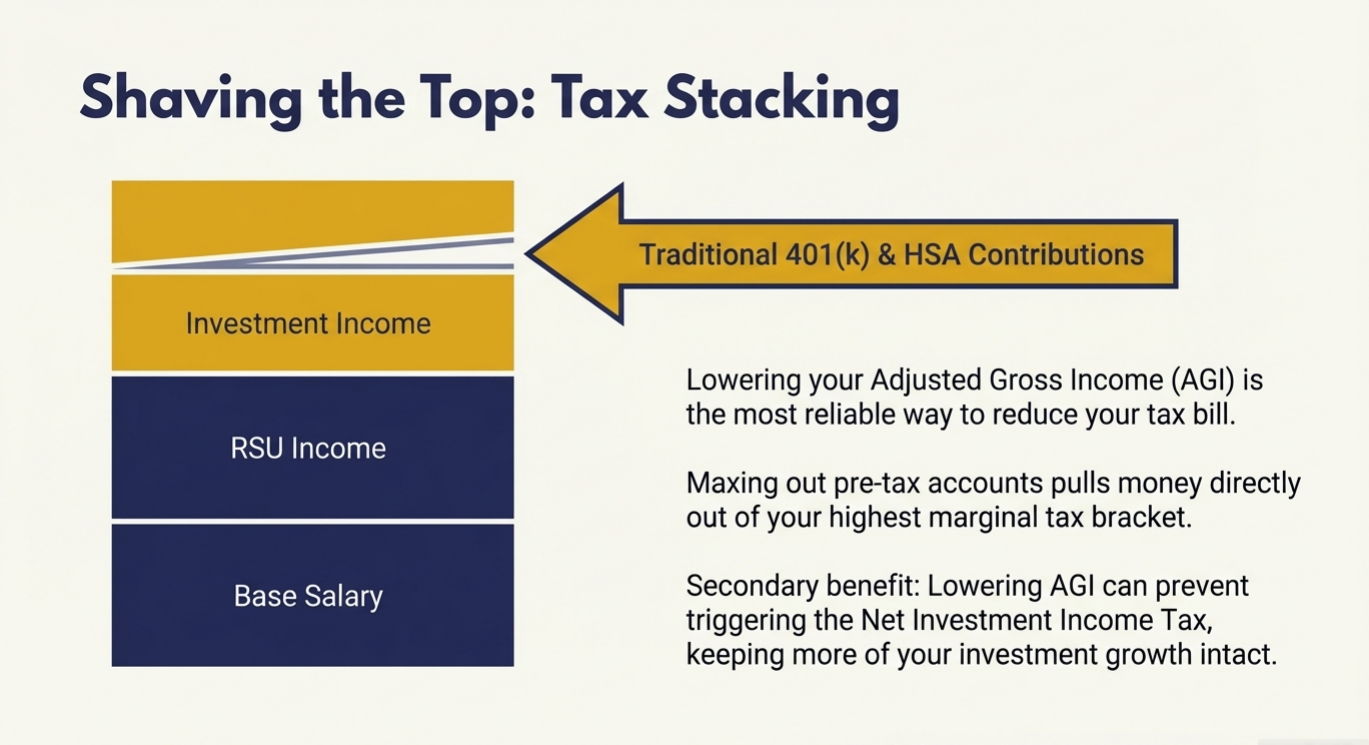

Lowering your Adjusted Gross Income is one of the most reliable ways to reduce your tax bill. Traditional 401 (k) contributions pull money out of your highest marginal tax bracket. Health Savings Account contributions offer the same benefit.

Managing your AGI provides secondary benefits. A lower income might prevent you from triggering the Net Investment Income Tax. This strategy keeps more of your investment growth in your pocket.

However, it's worth noting that maxing out pre-tax accounts comes with limitations. Funds inside a 401k are generally locked until age fifty nine and a half. Early withdrawals trigger a ten percent penalty. Health Savings Accounts require you to maintain a high-deductible health plan. These health plans expose you to higher out-of-pocket medical costs. All investments inside these accounts carry market risk and can lose value.

An income tax stacking infographic demonstrating how strategic financial planning tools directly reduce your adjusted gross income. The insight reveals how maximizing pre tax accounts pulls top earning dollars completely out of the highest marginal tax brackets.

Retirement and health savings account contributions are subject to federal limits and potential early withdrawal penalties.

Is Giving Concentrated Stock to Charity an Option?

High earners often hold too much of their own company's stock (in my opinion). Giving highly appreciated shares to charity solves two problems at once. You reduce your concentration risk while generating a valuable tax deduction. However, don't forget that this is for charitably inclined people. You will rarely end up with more money by giving it away, even if you get a tax benefit.

For those who are charitably inclined, a donor-advised fund serves as an excellent vehicle for this strategy. You transfer the appreciated shares directly into the fund. The IRS grants you a fair market value deduction for the year of the transfer. You can then sell the shares inside the fund without paying capital gains taxes. The money sits in the fund until you decide which charities to support.

You can learn more about managing single stock exposure in our post Diversifying Concentrated Stock with Less Tax.

Charitable giving requires careful consideration. Contributions to a donor-advised fund are irrevocable. You cannot take the money back if you experience a financial emergency. And tax deductions only benefit you if your total itemized deductions exceed the standard deduction.

When Should You Sell Your Vested RSUs?

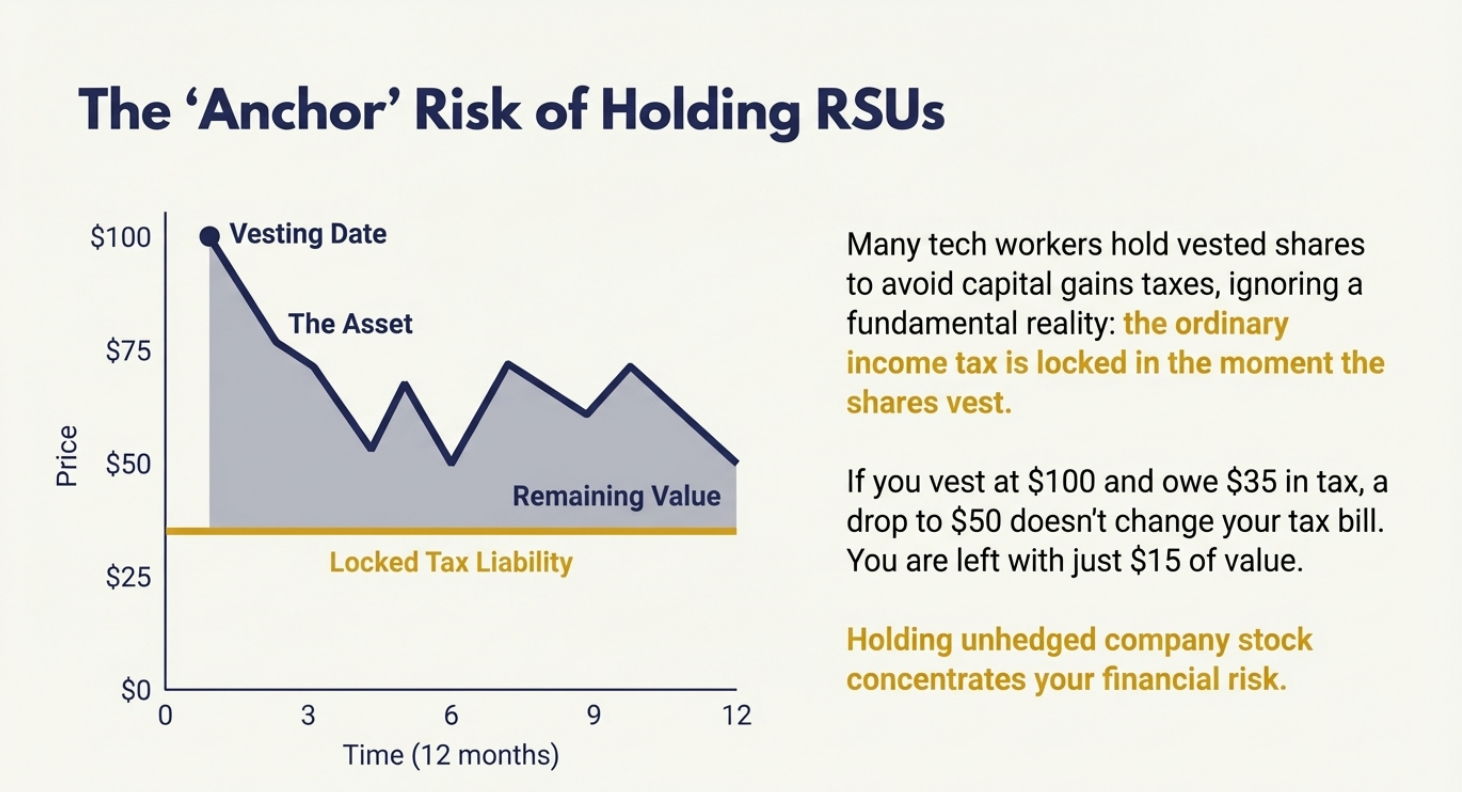

Many employees refuse to sell their vested shares. They tell themselves they want to avoid paying capital gains taxes. This mindset ignores a fundamental reality of equity compensation.

The ordinary income tax is already locked in the moment the shares vest. You owe tax on the vesting value regardless of what happens next. Holding the shares creates a new, separate tax and investment decision.

Imagine your shares vest at one hundred dollars. You owe thirty-five dollars in taxes. The stock drops to fifty dollars over the next six months. You still owe thirty-five dollars in taxes based on the vest price. Your remaining value shrinks to fifteen dollars.

Holding unhedged company stock concentrates your financial risk. Your salary and your investment portfolio rely on the same company. Selling RSUs immediately upon vesting is often a sound strategy and can remove a lot of this risk. But selling immediately does mean you might miss out on future price appreciation.

*All investments carry risk. Holding the stock exposes you to severe downside potential. You must evaluate your own liquidity needs and risk tolerance before deciding to hold concentrated equity.

A financial analysis line chart illustrating the anchor risk of holding vested equity. The key insight reveals that a post vest drop in stock price destroys net wealth because the original ordinary income tax liability remains permanently locked at the initial higher vest price.

All investments carry risk. This is a hypothetical illustration and does not reflect the performance of any specific asset.

FAQs

Why did my company only withhold twenty-two percent on my bonus?

The IRS classifies bonuses as supplemental income. Federal law mandates a flat twenty-two percent withholding rate for supplemental wages up to one million dollars. Your company simply followed the legal baseline requirement.

Can I ask my employer to withhold more taxes on my RSUs?

Yes. Some stock plan portals allow you to change your default sell-to-cover percentage. You can increase the withholding rate to match your actual marginal tax bracket. You can also file a new W-4 form to withhold extra cash from your regular paychecks.

Do I pay capital gains tax or ordinary income tax on RSUs?

You pay ordinary income tax on the total value of the shares on the day they vest. You only pay capital gains tax on any price appreciation that occurs after the vesting date.

What is the safe harbor rule for estimated taxes?

The safe harbor rule protects you from IRS underpayment penalties. High earners with an adjusted gross income over one hundred fifty thousand dollars must pay one hundred ten percent of their previous year's tax liability. Meeting this threshold waives the penalty even if you owe money in April.

Does a Mega Backdoor Roth help lower my taxes today?

No. Roth contributions use after-tax dollars. A Mega Backdoor Roth provides incredible tax-free growth for the future. It does not reduce your adjusted gross income or lower your current year tax bill.

Your Next Steps

- Review your most recent pay stub to calculate your current tax withholding trajectory.

- Compare the withheld amount against your projected total income. This highlights any immediate shortfall.

- Log in to your stock plan portal to see if you can adjust your default sell-to-cover percentage. Increase the rate if the platform allows custom elections. If not, you may have to adjust your W4 or make estimated tax payments.

Stop Letting the IRS Surprise You

Equity compensation should build your wealth rather than create constant tax anxiety. Waiting until April to plan for last year's equity vests virtually guarantees a stressful outcome. You deserve a clear path forward that protects your hard-earned money.

Let's talk about building a plan designed for tax efficiency. Schedule an introductory call today to learn more about our approach and determine if our services are a good fit for you.

To learn more about how we partner with clients, click here to view our services.

This blog is for educational purposes only and should not be taken as individual advice

–

Marcel Miu, CFA® and CFP® is the Founder and Lead Wealth Planner at Simplify Wealth Planning. Simplify Wealth Planning is dedicated to helping tech professionals master their money and achieve their financial goals.

This article first appeared on the Simplify Wealth Planning website and is republished on Flat Fee Advisors with permission.