Share this Post

If your ESPP feels like free money, read this first. Too many people lose their ESPP gains because they don’t have a selling plan. Here’s how to make sure that doesn’t happen to you.

Your ESPP Could Be a Wealth Killer

You enroll in your company’s Employee Stock Purchase Plan (what’s an ESPP?), buy shares at a discount, and watch the balance grow.

The numbers go up and it feels good.

So you let it ride. Maybe for tax reasons. Maybe because the stock is doing well. Maybe just because selling feels like giving up on potential upside.

Then the stock drops.

What was at one point a strategic financial move becomes a costly mistake. The gains you thought you locked in are now they’re gone. And worst of all, it was completely avoidable.

If you’ve been stacking ESPP shares without a selling plan, it’s time to fix that.

Most People Mess Up Their ESPP (And Don’t Even Know It)

Most ESPP participants focus on the purchase mechanics. They contribute every paycheck, trusting the system to deliver free money in the form of a discounted stock price.

The hard part isn’t buying ESPP shares. It’s what comes next.

When should you sell? How long should you hold? What about taxes?

Without a strategy, all your hard-earned ESPP gains can vanish.

Holding Too Long Can Backfire

Many people assume the smartest play is to hold their ESPP shares for at least two years to qualify for lower tax rates. In a perfect world, this works. You pay long-term capital gains tax on the increase instead of short-term rates.

But the market doesn’t care about your tax strategy.

Holding for longer only makes sense if the stock keeps rising. What if it actually drops? The tax benefits become meaningless because you're paying a lower tax rate on a lower profit. Or worse, a loss.

An ESPP is an opportunity. Not a guarantee.

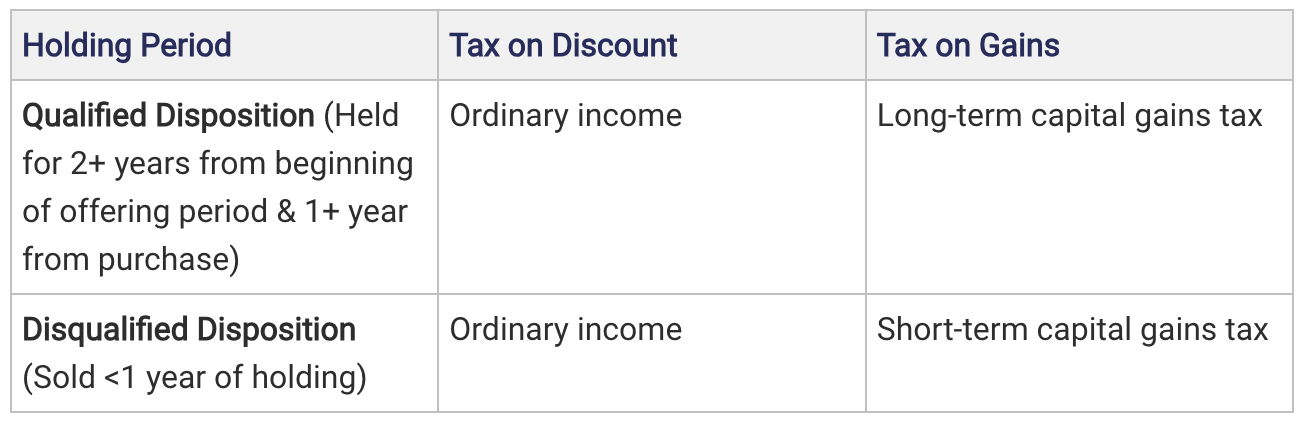

How ESPP Taxes Work

Qualified vs. Disqualified Dispositions (Learn More Here)

Selling ESPP shares triggers taxes, and the type of sale determines how much you owe.

At first glance, holding for the qualified disposition looks like the obvious choice. Less tax, more money, right?

Not always.

Sometimes, selling earlier, even at a higher tax rate, preserves more of your gains. If your stock price spikes, it’s worth considering cashing out rather than waiting for a better tax rate on a potentially much lower future value.

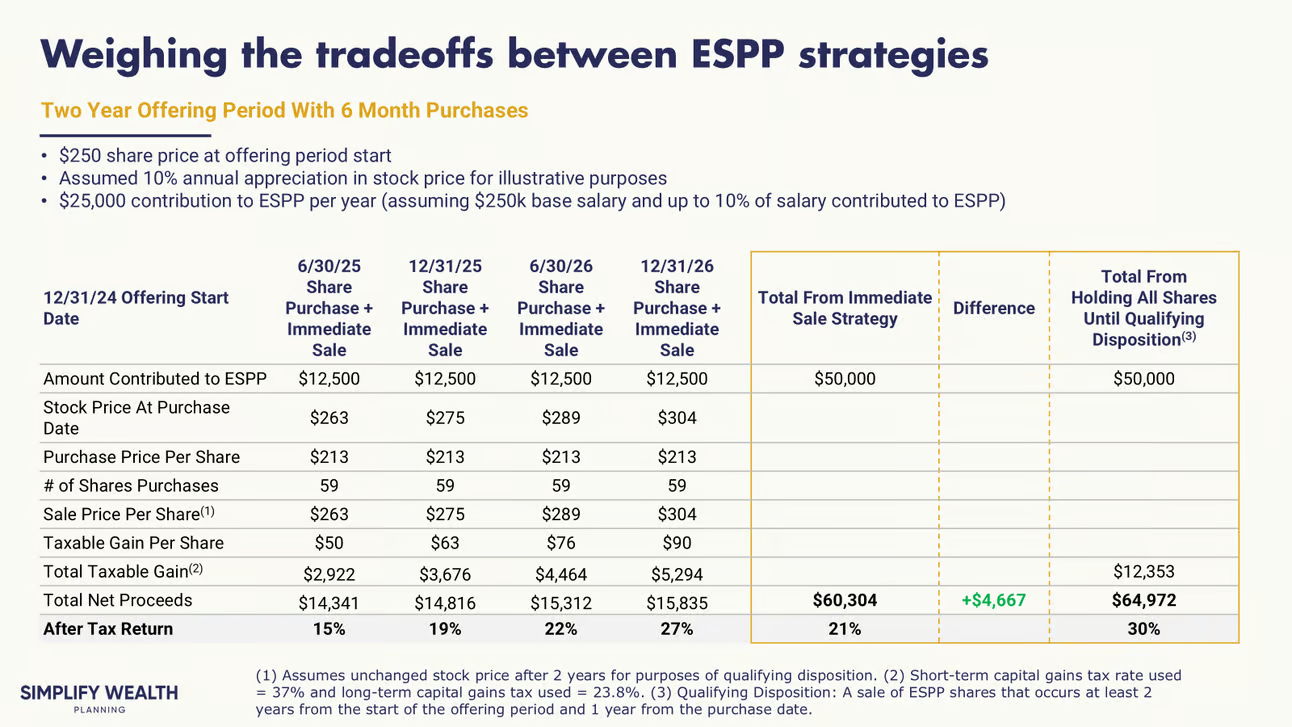

How much risk are you willing to take for the tax benefit? In the example below, you’re trading a guaranteed 21% after-tax return (which is phenomenal) for a chance to lock in a 30% gain.

Will it happen? Maybe. But don’t forget the old saying “pigs get fat and hogs get slaughtered.”

Your Next Steps: A Smarter ESPP Selling Plan

1. Calculate Your Company Stock Exposure

If more than 10-15% of your net worth is tied to your employer’s stock, you’re taking on too much risk. Even great companies stumble, and you don’t want your financial well-being crashing with them.

2. Plan for Future ESPP Purchases

Your ESPP contributions keep adding shares to your portfolio. That means even if your stock allocation looks fine today, it may not in a few years. Mapping out your estimated purchases helps you know when and how much to sell.

3. Use ESPP Proceeds for Strategic Goals

ESPP funds are real money. Using them to pay down debt, fund a home purchase, or invest in a diversified portfolio (why diversify?) can be a better move than simply holding for the sake of it.

4. Optimize for Taxes, But Don’t Let Taxes Dictate Your Choices

Yes, holding for a qualified disposition can reduce your tax bill. But waiting just to pay lower taxes only makes sense if the stock holds its value or continues rising. Make decisions based on total wealth, not just taxes owed.

5. Sell in Controlled Phases

Selling ESPP shares all at once can feel extreme. Instead, create a structured plan:

- Sell a percentage of shares every quarter or year

- Set automatic price-based sell triggers

- Offload just enough shares to offset ESPP tax liabilities

This gradual approach allows you to reduce risk without feeling like you're cashing out completely.

Meme Of The Week

Wrap-Up

An ESPP is a tool. That’s it. If it fits into your long-term strategy, great. If it doesn’t, adjust.

The biggest mistake is not having a plan at all.

Most people don’t realize their stock exposure risk until it’s too late. A little proactive management today can prevent a painful financial lesson tomorrow.

Not sure what to do with your ESPP? Let’s talk.

–

Marcel Miu, CFA, CFP is the Founder and Lead Wealth Planner at Simplify Wealth Planning. Simplify Wealth Planning is dedicated to helping tech professionals master their money and achieve their financial goals.

This article first appeared on the Simplify Wealth Planning website and is republished on Flat Fee Advisors with permission.